Why a Generic Will Won’t Protect High-Net-Worth Assets

You wouldn’t trust a discount-store reading glass prescription for a complex eye condition. A poorly drafted estate plan can cost a high-net-worth family $200,000–$500,000 in unnecessary taxes, probate fees, and litigation—often more than the cost of a comprehensive plan.

A generic will does nothing to shield assets from estate tax, generation-skipping transfer tax, or creditors. It guarantees probate, which in states like California or New York can drag on for 12–18 months and eat 3–7% of gross asset value in fees. Worse, it offers zero protection against family disputes: a simple “I leave everything to my children” becomes a legal battlefield when blended families, special-needs beneficiaries, or business-succession complexities exist.

Specialized trust and estate law firms build customized strategies—GRATs, FLPs, dynasty trusts, charitable remainder trusts—that are legally unattainable with off-the-shelf documents. They model your tax exposure under current law, coordinate with your CPA and financial advisor, and update your plan as life and legislation change. One missed trust-funding step or outdated marital-deduction clause can cost your heirs their inheritance—or hand it to the IRS.

The Core Services a Trust and Estate Law Firm Should Offer

Think of a trust and estate law firm as the quarterback of your wealth-transfer team. A full-service firm doesn’t just draft a will—it builds a layered strategy that addresses taxes, asset protection, and family dynamics simultaneously.

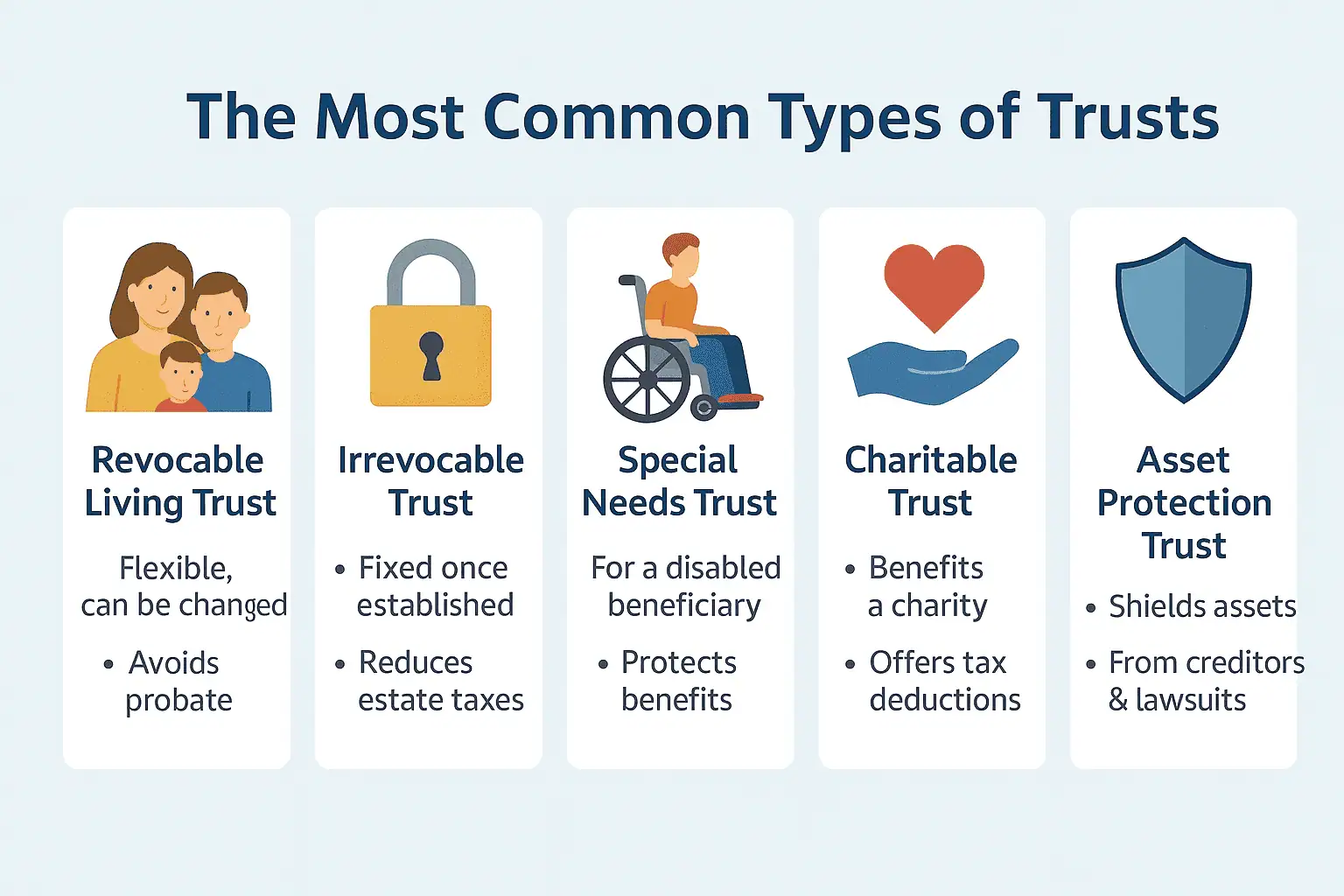

At minimum, the firm should handle the foundational documents: wills, revocable living trusts, durable powers of attorney, and healthcare directives. For high-net-worth clients, that’s table stakes. The difference shows up in the advanced toolkit. Look for a firm that regularly structures GRATs, FLPs, CRTs, and dynasty trusts. Failure to properly fund and administer a dynasty trust alone can cost a family millions in lost tax benefits over two generations.

The firm should also handle probate administration—not just planning, but the execution when a client dies. Because the IRS audits roughly 10–15% of large estates (those over $10 million), your firm needs to be fluent in estate, gift, and generation-skipping transfer (GST) tax planning.

Finally, the best firms coordinate with your CPA and financial advisor. If your attorney works in a silo, you’re paying for a plan that may contradict your tax strategy or trigger unintended capital gains. A firm that insists on joint meetings isn’t being pushy—they’re being thorough.

How to Verify a Firm’s Expertise in Tax-Efficient Planning

You wouldn’t hire a general practitioner for open-heart surgery. Start by looking for credentials that signal serious specialization. Board certification in estate planning or tax law is a strong indicator, but the gold standard is membership in the American College of Trust and Estate Counsel (ACTEC)—an invitation-only organization that admits fewer than 1% of practicing attorneys based on peer-reviewed expertise.

Then, press for specifics. Ask how many Form 706 (estate tax) returns the firm has filed in the last two years, and whether they regularly structure GST tax strategies. A firm that handles fewer than a handful of 706 filings annually likely lacks depth for complex, high-asset situations. Estates exceeding the current federal exemption threshold—$13.61 million per individual as of 2026—trigger filing requirements, and penalties for errors can be steep.

Finally, audit their thought leadership. A firm that publishes detailed articles, speaks at industry conferences, or releases case studies on strategies like GRATs, FLPs, or dynasty trusts signals that they live in this space. If their website only offers generic “what is a will” content, they’re likely not the right partner for tax-efficient wealth transfer.

Red Flags to Avoid When Vetting a Trust and Estate Law Firm

The first red flag is a lack of specialization. Estate planning attorneys typically command billable rates of $400–$800 per hour—you’re paying for expertise, not a generalist who will Google the tax code while you wait.

Next, watch for the “one-size-fits-all” pitch. If a firm pushes a revocable living trust as the only solution without asking about your business assets, family dynamics, or estate tax exposure—run. Nearly 60% of affluent families who later faced litigation had initial plans that used generic templates, missing crucial provisions for asset protection or generation-skipping transfer taxes. The right firm should explore alternatives like GRATs, FLPs, or dynasty trusts, depending on your numbers.

Finally, ask about their update process. If the attorney shrugs when you ask how your plan adapts to tax law changes or a future divorce, that’s a dealbreaker. The American Bar Association recommends a formal review every three years or after any major life event. A firm that can’t articulate a clear revision timeline is selling you a static document, not a living strategy.

Choosing Between Local Boutique Firms and National Practices

When a Local Boutique Firm Wins

A small, specialized firm can be your best ally if your wealth is concentrated in one state. They know that state’s specific laws—whether it’s California’s community property rules, Florida’s homestead protections, or New York’s estate tax threshold (currently $6.94 million, indexed for inflation). You get the partner’s direct cell number, and they’ll know the local probate judges by name. Over 60% of estate planning attorneys in boutique firms report that personalized, ongoing client relationships are their primary competitive advantage.

When a National Practice Makes Sense

If you own property in three states, run a business with international operations, or have a blended family that could trigger litigation, a national firm’s bench depth is invaluable. They can deploy a team with specialists in tax, corporate law, and litigation—often within 24 hours.

The Decision Framework

- Asset complexity: Single-state real estate and standard investment accounts → boutique. Multi-state properties, private equity stakes, or foreign assets → national.

- Family geography: All heirs in one state → boutique. Heirs scattered across jurisdictions with different tax regimes → national.

- Ongoing tax needs: Simple annual gifting → boutique. GRATs, CRTs, or dynasty trusts requiring continuous tax strategy → national.

Neither option is universally better. The right choice aligns your legal counsel’s bandwidth and expertise with the actual shape of your wealth.

What Experts Recommend for Your Initial Consultation

Think of your first meeting as a diagnostic exam where you control the chart. Start with a one-page net worth summary—assets, liabilities, and ownership structures (LLCs, partnerships, real estate holdings). Attach a list of your intended beneficiaries and any existing wills, trusts, or prior estate documents. Nearly 60% of high-net-worth families who experienced estate litigation had outdated or incomplete beneficiary designations. That single page can save you from becoming a statistic.

Then, ask three specific questions to separate the specialists from the generalists:

- “How do you structure trusts to minimize GST tax?” If they can’t explain dynasty trust mechanics or generation-skipping transfer tax exemptions in plain terms, that’s a red flag.

- “What is your experience with business succession?” For business owners, a generic will is a liability. You need a firm that has handled buy-sell agreements and valuation freezes.

- “How often should we review the plan?” The right answer isn’t “once” or “every ten years.” It’s “annually, or after any major life event—marriage, divorce, business sale, or tax law change.”

Finally, gauge their communication style. If they lean on jargon (“QTIP trusts,” “GRATs”) without checking your understanding, they’re showing you how they’ll communicate with your family later—poorly. A sophisticated firm explains complex concepts in clear, actionable language. If you leave the consultation more confused than when you arrived, keep looking.

When to Escalate or Seek a Second Opinion

Even after you’ve chosen a firm, a quiet doubt might linger: Is this plan sophisticated enough for what I actually own? Trust that instinct. Nearly 70% of high-net-worth families who litigate estates do so because the original plan didn’t account for a specific asset or family dynamic—not because the assets were gone.

You should escalate or seek a second opinion when the proposed plan feels like a template. If your attorney can’t articulate the tax trade-offs between a GRAT and a sale to an intentionally defective grantor trust, or if they brush off your question about generation-skipping transfer taxes, that’s a red flag. A one-size-fits-all will or a simple revocable trust is rarely sufficient when you hold business interests, real estate in multiple states, or assets approaching the current federal estate tax exemption ($13.61 million per individual as of 2026).

Specific situations demand escalation:

- Blended families – A standard plan can unintentionally disinherit children from a first marriage.

- Special needs beneficiaries – A poorly drafted trust can jeopardize government benefits.

- International assets – U.S.-only counsel may miss foreign tax treaties or forced heirship laws.

- A pending business exit – The structure of your trust should align with the sale timeline to avoid a catastrophic tax event.

Your best safety net is a second review from a tax attorney or CPA who specializes in high-net-worth estates. Expect to pay $2,500–$7,500 for a comprehensive critique of the proposed plan—a fraction of the cost of fixing a mistake in probate or during an IRS audit. A confident firm will welcome the scrutiny; a defensive one just confirmed your doubt.

How to Evaluate Ongoing Relationship and Plan Updates

An estate plan isn’t a “set it and forget it” document—it’s a living strategy that needs to evolve with your life and the tax code. Nearly 60% of wealthy families who experience a significant tax law change fail to update their estate plans within the first year, often costing them millions in unnecessary taxes. So before you hire a firm, ask about their process for ongoing relationship management, not just the initial plan creation.

First, confirm whether the firm conducts annual or periodic reviews—ideally on a proactive calendar, not only when you call. This is critical as of 2026, with the Tax Cuts and Jobs Act provisions set to sunset at the end of 2025, potentially slashing the federal estate tax exemption from roughly $13.6 million per individual to around $7 million. A firm that doesn’t flag this change for you is a liability, not a partner.

Second, ask about attorney continuity. Will the same senior attorney handle your updates and any trust administration down the road, or will you be passed to junior staff after the initial signing? Consistency matters: a partner who knows your family dynamics, business structure, and prior intent can spot a looming issue in a five-minute phone call that a new associate might miss entirely. Look for a firm that guarantees your primary contact for at least the first three years of the relationship.